Understanding Insurance: Protecting Your Future and Financial Assets

Grasping insurance concepts is essential for anyone looking to protect their financial future. Insurance offers a safeguard against unexpected events potentially causing substantial damage. Various types of coverage exist, suited to various individual necessities. Yet, numerous people find it difficult deciding on the appropriate level of protection and navigating the specifics of their policy. The complexities of insurance can create uncertainty, prompting the need for a clearer understanding on how best to protect one's wealth. What must someone think about before committing to a policy?

The Basics of Insurance: What You Need to Know

Insurance functions as a monetary safeguard, shielding people and companies from unanticipated hazards. It is essentially an agreement between the insured and the insurer, in which the policyholder remits a fee for receiving fiscal security covering defined damages or setbacks. The primary function of coverage is managing exposure, enabling people to shift the responsibility of possible monetary damage onto a provider.

Coverage agreements detail the rules and stipulations, specifying the scope of protection, which situations are not covered, along with the process for submitting claims. Resource pooling is fundamental to coverage; a large number of participants pay in, making it possible to finance payouts to those who incur damages. Grasping the core concepts and language is crucial for choosing wisely. In sum, coverage aims to offer security, making certain that, when disaster strikes, individuals and businesses can recover and continue to thrive.

Types of Insurance: An Extensive Look

Many different kinds of insurance exist to address the wide-ranging necessities for people and companies alike. Among the most common are health insurance, designed to handle doctor bills; motor insurance, shielding against automobile harm; as well as property coverage, securing assets from perils such as theft and fire. Life coverage provides monetary protection to beneficiaries in the event of the policyholder's death, whereas income protection offers salary substitution if one becomes unable to work.

For businesses, liability insurance protects against claims of negligence, and asset insurance secures physical holdings. Professional liability coverage, also known as E&O insurance, protects professionals from lawsuits stemming from omissions in their services. Furthermore, travel insurance provides coverage for unexpected events during trips. Each type of insurance plays an essential role in managing risks, allowing individuals and businesses to lessen potential economic harm and keep things stable when conditions are uncertain.

Determining What Insurance You Need: What Amount of Insurance Do You Require?

Determining the appropriate level of necessary protection demands a detailed review of property value and possible dangers. Individuals must assess their monetary standing and the property they want to safeguard to reach a sufficient level of coverage. Sound risk evaluation methods are fundamental to ensuring that one is not lacking enough coverage nor spending too much on superfluous insurance.

Determining Property Value

Determining asset valuation is a crucial stage in knowing the required level of protection for sound insurance safeguarding. This process involves determining the worth of private possessions, land and buildings, and monetary holdings. Those who own homes need to weigh things such as today's market situation, reconstruction expenses, and depreciation when valuing their home. In addition, people need to assess private possessions, cars and trucks, and possible legal dangers connected to their property. Through creating a comprehensive list and appraisal, they can identify possible holes in their protection. In addition, this evaluation helps individuals adjust their coverage to address particular needs, ensuring adequate protection against unanticipated incidents. Ultimately, accurately evaluating asset value lays the foundation for prudent insurance planning and financial security.

Risk Assessment Strategies

Gaining a comprehensive grasp of asset worth logically progresses to the following stage: determining necessary insurance. Risk assessment strategies involve identifying potential risks and establishing the necessary amount of protection required to mitigate those risks. The procedure starts with a full accounting of property, such as real estate, automobiles, and private possessions, alongside an analysis of potential liabilities. The person needs to evaluate elements like location, daily habits, and risks relevant to their profession that could impact their insurance requirements. Furthermore, checking existing coverage and pinpointing missing protection is essential. By measuring potential risks and aligning them with the value of assets, you can make educated choices about the required insurance type and quantity to safeguard their future effectively.

Understanding Policy Terms: Essential Ideas Clarified

Grasping the language of policies is crucial for traversing the complexities of insurance. Important principles such as coverage categories, premiums, out-of-pocket limits, policy limits, and limitations play significant roles in judging how well a policy works. A solid understanding of these terms allows people to make educated choices when choosing coverage plans.

Types of Coverage Defined

Coverage options offer a selection of different coverages, all created to handle specific risks and needs. Common types include liability coverage, which protects against legal claims; property coverage, safeguarding physical assets; and coverage for personal injury, which addresses injuries sustained by others on one’s property. Additionally, extensive coverage offers protection against a broad spectrum of dangers, including theft and natural disasters. Specialized coverages, such as professional liability for businesses and health insurance for individuals, adjust the security provided. Knowing these coverages enables insured parties to pick suitable coverage based on their unique circumstances, ensuring adequate protection against potential financial losses. Every coverage category is vital in a comprehensive coverage plan, leading to monetary safety and serenity.

Insurance Costs and Out-of-Pocket Limits

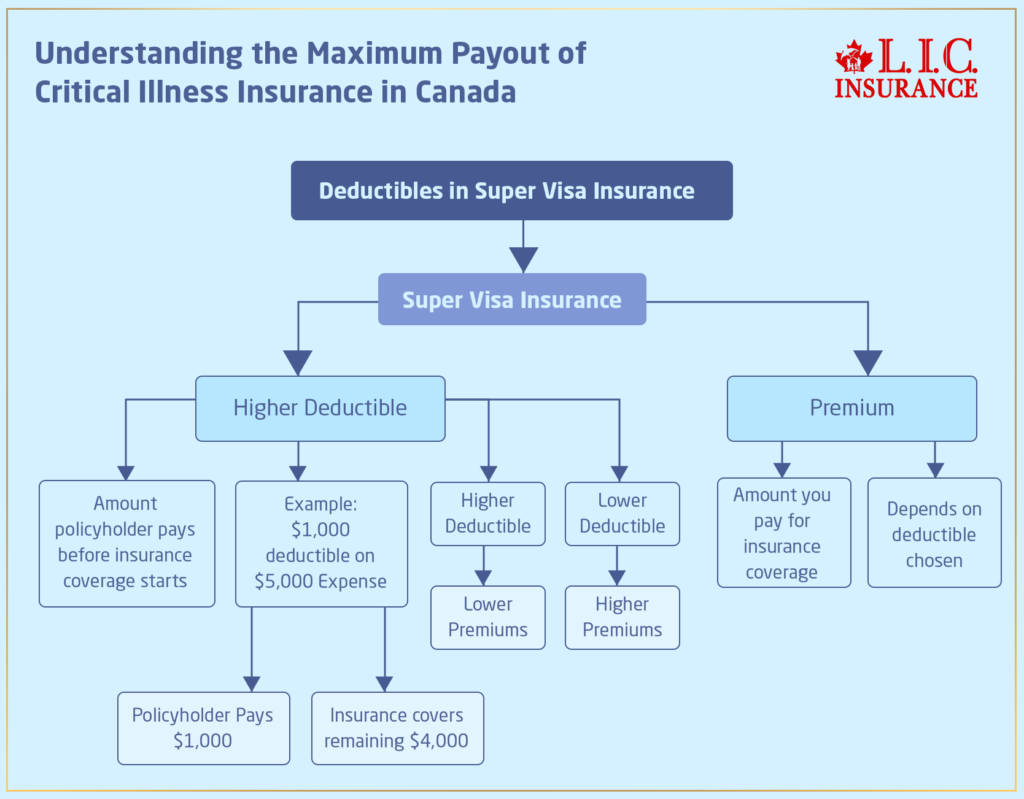

Choosing the appropriate coverage categories is only part of the insurance equation; the financial components of premiums and deductibles also greatly influence policy decisions. The premium is the fee for holding an insurance policy, generally paid on an annual or monthly basis. A larger premium usually corresponds to more extensive coverage or lower deductibles. In contrast, deductibles are the amounts policyholders must pay out-of-pocket before their policy protection activates. Choosing a higher deductible often decreases premium expenses, but it may lead to greater financial responsibility during claims. Understanding the balance between these two elements is essential for individuals seeking to secure their holdings while managing their budgets effectively. In the end, the relationship of deductibles and premiums defines the overall value of an insurance policy.

Limitations and Exclusions

Which factors that can limit the effectiveness of an insurance policy? Restrictions and caveats within a policy specify the conditions under which coverage is withheld. Examples of exclusions include pre-existing conditions, war-related incidents, and specific natural catastrophes. Limitations may also apply to specific coverage amounts, making it essential for policyholders to recognize these restrictions thoroughly. These elements can greatly influence payouts, as they specify what losses or damages will not be paid for. It is vital that policyholders examine their insurance contracts carefully to spot these limitations and exclusions, so they are well aware about the extent of their coverage. Proper understanding of these terms is essential for effective asset protection and future financial planning.

Filing a Claim: What to Expect When Filing

Filing a claim can often seem daunting, especially for those unfamiliar with the process. The starting point typically involves notifying the insurance company of the incident. This can usually be done through a phone call or digital platform. After the claim is filed, an adjuster may be designated to review the situation. This adjuster will review the details, collect required paperwork, and may even inspect the location of the event.

Following the evaluation, the insurer will determine the validity of the claim and the payout amount, based on the policy terms. Those filing should be prepared to offer supporting evidence, such as receipts or photos, to help the review process. Communication is essential throughout this process; the insured might need to check in with the insurer for updates. Ultimately, understanding the claims process helps policyholders navigate their rights and responsibilities, to guarantee they obtain the funds they deserve in a prompt fashion.

Guidelines for Finding the Right Insurance Provider

How does one find the most suitable insurance provider for their situation? To begin, people must evaluate their unique necessities, looking at aspects such as the kind of coverage and financial limitations. It is crucial to perform comprehensive research; online reviews, evaluations, and client feedback can provide insights into customer satisfaction and the standard of service. In addition, obtaining quotes from multiple providers makes it possible to contrast premiums and the fine print.

It is also advisable to evaluate the financial stability and credibility of potential insurers, as this can impact their ability to fulfill claims. Speaking directly to representatives can make the terms and conditions of the policy clearer, guaranteeing openness. Moreover, seeing if any price reductions apply or combined offerings can enhance the overall value. Lastly, getting suggestions from people you trust may lead to discovering dependable choices. By following these steps, individuals can make informed decisions that are consistent with their insurance needs and budgetary aims.

Staying Informed: Ensuring Your Policy Stays Relevant

After picking the best coverage company, individuals must remain proactive about their coverage to guarantee it meets their evolving needs. Regularly reviewing policy details is essential, as life changes—such as marriage, acquiring property, or career shifts—can impact coverage requirements. Policyholders must plan annual reviews with their insurance agents to talk about necessary changes based on these personal milestones.

In addition, remaining aware of industry trends and updates to insurance laws can provide valuable insights. This knowledge may reveal new insurance possibilities or discounts that could make their policies better.

Keeping an eye on the market for better prices may also result in cheaper options without sacrificing protection.

Questions People Often Ask

How Are Insurance Rates Affected With Age and Location?

Insurance premiums typically increase with age due to increased risks associated with older individuals. Furthermore, geographic area influences costs, as urban areas often experience higher premiums due to increased exposure to accidents and theft compared to non-urban locations.

Can I Change my insurance company in the middle of the term?

Absolutely, people are able to switch their coverage provider mid-term, but it is necessary to check the conditions of their existing coverage and guarantee they have new coverage in place to avoid gaps in protection or associated charges.

What are the consequences of missing a insurance installment?

If an individual misses a premium payment, their insurance coverage may lapse, leading to potential loss of protection. It may be possible to reinstate the policy, but may necessitate paying outstanding premiums and may involve penalties or more expensive coverage.

Do pre-existing medical issues qualify for coverage in health plans?

Pre-existing conditions may be covered in health plans, but the inclusion depends on the specific plan. Numerous providers enforce a waiting time or specific exclusions, whereas some offer instant protection, emphasizing the importance of reviewing policy details corresponding information thoroughly.

How Do Deductibles Affect the cost of my coverage?

Deductibles affect the price of insurance by establishing the figure a holder of the policy is required to spend before the plan begins paying. If deductibles are higher, monthly premiums are usually lower, and a smaller deductible causes higher payments and potentially reduced personal spending.